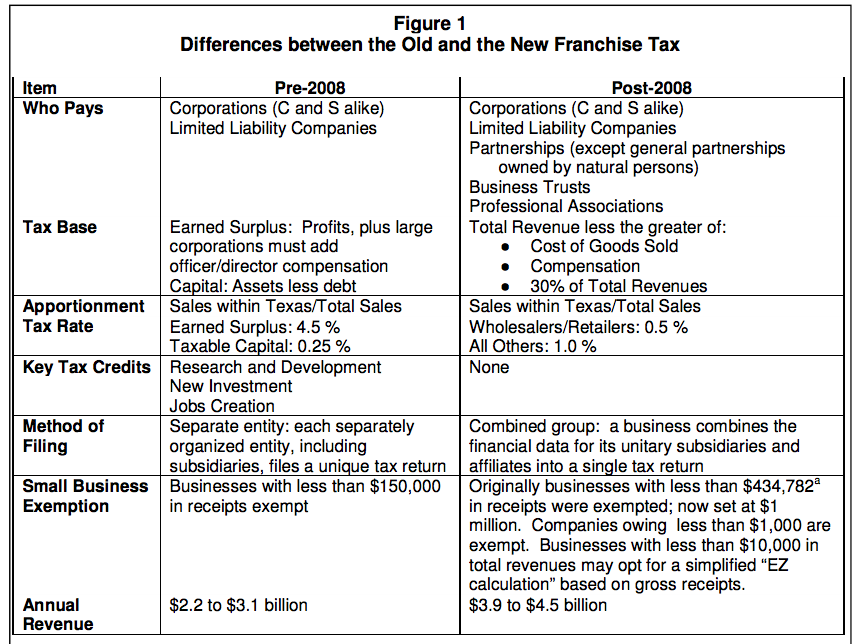

Who It Applies To

The franchise tax is imposed on each corporation that is chartered in Texas. Non-Texas corporations doing business in Texas are also liable for the tax. For franchise tax purposes, the term "corporation" also includes a bank, state limited banking association, savings and loan association, limited liability company, limited partnership, professional limited liability company, a corporation that elects to be an S corporation for federal income tax purposes, and a professional corporation. However, professional associations and general partnerships are not subject to the franchise tax.

Exemptions

All organizations claiming an exemption must file an application to the Comptroller. The burden of proof is on the organization filing for exemption. Eligible organizations include:

You can file an application for exemption here.

All organizations claiming an exemption must file an application to the Comptroller. The burden of proof is on the organization filing for exemption. Eligible organizations include:

- Entities subject to insurance premium taxes

- Organizations responsible for the promotion of public interest

- Non-profit organizations that hold a 501(c) status

- Homeowner's Associations

- Passing entities

You can file an application for exemption here.

Loopholes

- “Delaware Sub”: a company places its Texas operations into a partnership and creates an out-of-state corporate subsidiary as a limited partner. Neither the partnership nor the out-of-state limited partner were subject to Texas franchise tax, sharply reducing the overall amount of tax due. This structure received much scrutiny when a few publicly-traded companies took advantage of it, but it was also commonly used by medium- and smaller-sized companies.

- “Geoffrey’s Sub”: a company creates an out-of-state subsidiary as owner of intangible property, such as trademarks and patents. The amount a Texas company was charged for the use of these properties was a deduction against their franchise tax, but the income to the out-of- state subsidiary was not subject to tax.

- Profit Shifting: certain smaller corporations did not have to add the amount of compensation paid to their company officers and directors to their tax base (as large corporations did). These businesses could pay their earnings as compensation to their officer-director owners, essentially converting profit into a deductible business expense.