How To Calculate It

Taxing on a Business's Margin

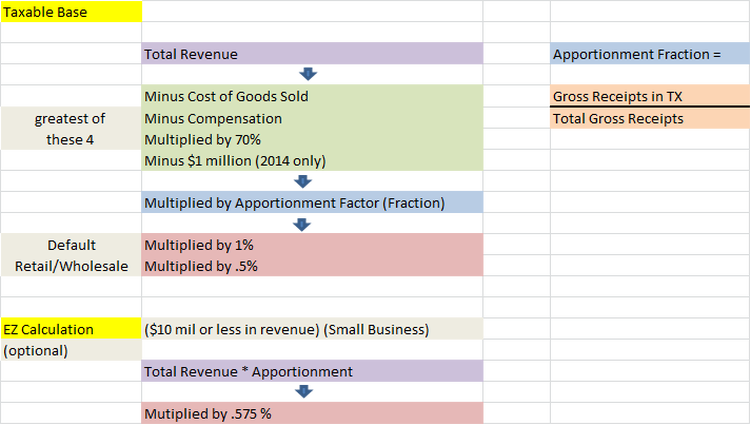

The tax base is the taxable entity's margin, except for entities that file the EZ Computation. Margin equals the least of four calculations based on eligibility:

o Total revenue minus cost of goods sold

o Total revenue minus compensation

o 70 percent of total revenue

o (for reports originally due on or after Jan. 1, 2014) total revenue minus $1 million.

Total Revenue

Total revenue is determined from revenue amounts reported for federal income tax minus statutory exclusions. Exclusions from revenue include the following:

Cost of Goods Sold

Cost of goods sold generally includes costs related to the acquisition and production of tangible personal property and real property. Taxable entities that only sell services will not generally have a cost of goods sold deduction.

Compensation

Is wages, benefits and compensation paid to employees, owners and partners in a 12-month pay period. Subject to per person limitation of $300,000 and adjusted for inflation. Does not include labor or payroll taxes.

Apportionment

The taxable margin is multiplied by the apportionment factor to account for the reasonable percentage of business activity that can be attributed to the state.

The factor or fraction is:

Gross Receipts in Texas / Total Gross Receipts for Entire Business

Tax Rate

TAX Rate for Reports in 2014

· 0.975 percent for most taxable entities

· 0.4875 percent retailers or wholesalers

TAX Rate for Reports 2008-2013

· 1 percent for most taxable entities

· 0.5 percent for retailers and wholesalers

An entity is considered a retail or wholesale entity if trade if its total revenue from activities in retail and wholesale trade is greater than total revenue from activities in trades other than retail and wholesale trade.

EZ Computation

A taxable entity with annualized total revenue of $10 million or less can has to the option to calculate the franchise tax by multiplying total revenue by the apportionment factor and then multiplying the apportioned total revenue by a tax rate of 0.575 percent (.00575).

A taxable entity that elects to use the EZ computation cannot deduct the cost of goods sold, the compensation the 70 percent of total revenue, or the $1 million deduction from its margin.

Would make the most sense if you were a small business owner that makes less than $10 million in annual revenue, not a retailer or wholesaler and would not have large deductions (compensation, COGS) from your taxable base.

No Tax Due

You are not due any franchise Tax if:

· Your annualized total revenue is below the no-tax-due threshold of:

- $1 million* or less for reports after 2010

- $300,000 or less for reports before 2010

*Number is approximate. Increases by small increments every two years to adjust for inflation. (Threshold is $1,080,000 for 2014-2016)

All taxable entities, including those that owe no tax, must file a report. All taxable entities, except passive entities, must also file either a Public Information Report or an Ownership Information Report.

The law imposes a $50 penalty if a franchise tax report is filed late even if no tax is due with that report.

Problems with the calculation

One issue with taxes like the Texas Franchise tax that business owners need to know about is how gross receipts taxes are not neutral. They actually tend to have lower effective rates on industries with fewer stages of production and higher effective rates on industries with more stages of production. The tax becomes embedded in the price of products that go through two or more stages from one business to another.

For example, if you build a car under a gross receipts tax regime, the rubber in the tire would be taxed when it came out of the tree and was sold to the tire company, then again when the tire company sells the tire to the car manufacturer, then a third time when the car manufacturer sells to the consumer.

Owners of business’s with several stages of production should be aware of this.